The question isn't whether a 1% rate drop is a good deal. It's how many months it will take for your monthly savings to cover your closing costs — and whether you plan to stay in the house that long. If you don't stay past your break-even point, you didn't save money; you just paid your lender to lower your rate.

When you're anxious about high rates, it's easy to focus on the monthly payment and ignore the upfront fees. But a lower payment doesn't automatically mean a better financial decision.

Here is exactly how to run the numbers to see if a refinance actually makes sense for you.

Why the "1% Rate Drop" Rule Is Useless

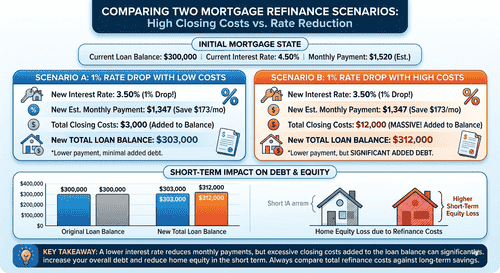

For decades, the standard advice has been to wait until mortgage rates drop at least 1% before refinancing. But this rule of thumb is fundamentally flawed because it entirely ignores closing costs.

A 1% drop could save you $200 a month. But if your lender charges $12,000 in closing costs, it will take you 60 months (five full years) just to break even. If you sell the house or refinance again in year three, you lost money on the deal. The interest rate doesn't matter if the upfront costs erase your savings.

The Only Formula You Need: The Break-Even Point

The true test of a refinance is dividing your total closing costs by your monthly savings.

This tells you exactly how many months it will take to recover your costs. If your closing costs are $10,524 and your new rate saves you $300 a month, the math is $10,524 ÷ $300=35 months.

Plug your numbers into the break-even calculator — it will give you the exact month you come out ahead, factoring in your specific loan balance and fees.

The Three Hidden Traps Lenders Don't Highlight

Even if your break-even point looks good on paper, there are three common traps that can make a refinance more expensive over the long run.

1. Resetting the Clock to 30 Years

When you are five years into a 30-year mortgage and you refinance into a new 30-year loan, you are extending your total payoff time to 35 years. Even with a lower interest rate, paying interest for an extra five years often means you pay more total interest over the life of the loan.

2. Rolling Closing Costs into the Loan

Lenders often pitch a "no out-of-pocket" refinance by rolling the closing costs into your new loan balance. You don't bring cash to closing, but you are now paying interest on your own closing costs for the next 30 years. Your $300,000 mortgage just became a $310,000 mortgage.

3. Buying Points in a Declining Rate Environment

Discount points allow you to pay cash upfront to lower your rate. But as one of the top comments in the r/Mortgages community warns: "Say it with me — I will not buy points in a declining rate environment!" If rates are expected to drop further over the next year or two, you might want to refinance again. If you do, the thousands of dollars you spent buying points on the first refinance are gone forever.

Running the Numbers: A Real Example

Let's look at a real scenario shared recently on Reddit. A homeowner was offered a rate drop from 7.5% to 5.875%, but with $10,524 in closing costs.

Their original payment was $2,796. The new payment would be $2,367. That is a monthly savings of $429.

The formula is $10,524 ÷ $429=24.5 months.

If they plan to stay in the home for at least two and a half years, this is a mathematically sound decision. If they might move next year, they should keep their 7.5% rate.

When a No-Cost Refinance Makes Sense

A "no-cost" refinance doesn't mean there are no closing costs; it means the lender pays them for you. In exchange, you get a slightly higher interest rate than you would if you paid the fees yourself.

This strategy makes perfect sense if you think rates will drop again soon. You accept a modest rate reduction today with zero break-even period. If rates drop another 1% next year, you can refinance again without having wasted thousands on sunk closing costs.

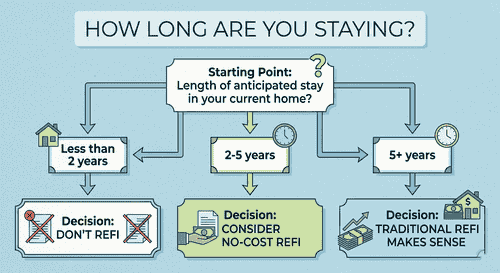

The "How Long Are You Staying" Decision Tree

The break-even math ultimately forces you to answer one question: how long are you staying? This is the exact same logic you use when comparing an ARM vs. Fixed Rate Mortgage.

- If you are selling in 1–2 years: Do not refinance. You will never recover the closing costs.

- If you are staying 3–5 years: Look closely at the break-even point. A no-cost refinance might be the safest bet.

- If this is your forever home: Pay the closing costs to secure the lowest possible fixed rate, because you have decades to reap the savings.

15-Year vs. 30-Year Refinance: Different Logic Entirely

If you are refinancing from a 30-year to a 15-year mortgage, the standard break-even formula breaks down.

Your monthly payment will likely go up, not down, because you are compressing your repayment window. You aren't doing this for monthly cash flow; you are doing it to save tens of thousands of dollars in lifetime interest. In this scenario, you look at the total interest paid over 15 years versus the remaining interest on your current loan, rather than monthly savings.

Stop guessing and run your own scenario. Use the break-even calculator to see exactly how your closing costs and new rate impact your financial future.