Your rate didn't change — this is your escrow account catching up with your actual property tax bill or insurance premium. When taxes or insurance go up, your lender pays the higher bill on your behalf, which empties your escrow account faster than expected. Now, they are raising your monthly payment to cover the new higher bills going forward, and to repay the shortage from last year.

Take a deep breath. This is completely normal, it is legal, and part of it is temporary.

Your Rate Didn't Change — Your Escrow Did

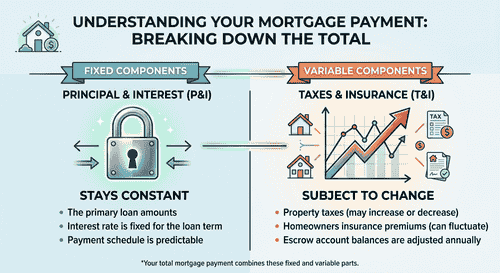

To understand why your payment jumped, you need to understand what an escrow account actually does. Every month, your mortgage payment is split into two buckets. The first bucket pays your loan principal and interest — this amount never changes if you have a fixed-rate mortgage.

The second bucket goes into your escrow account. Think of escrow as a forced savings account managed by your lender. They use this money to pay your property taxes and homeowners insurance for you when those bills are due. But your lender is only guessing what those bills will be based on last year. If your city reassesses your property value and your taxes go up, or if your insurance company hikes your premium, the lender still pays the bill so you don't lose your house. However, this creates an escrow shortage.

The Math: How Your Lender Calculates the Shortage

When an escrow shortage happens, your lender doesn't just ask you for a one-time check (though you can usually choose to pay it that way). Instead, they spread the shortage over the next 12 months.

Additionally, federal law (RESPA) allows lenders to keep a two-month cushion in your account. This cushion acts as a buffer so they don't bounce a check if your taxes go up again. When your core tax bill increases, the required two-month cushion increases too, which adds slightly more to your shortage.

Let's look at a real example. Imagine your property tax bill was $3,600 last year, so your lender was collecting $300 a month. This year, your tax bill jumps to $5,400.

First, your new monthly escrow collection must increase by $150 to cover the new $5,400 bill ($450/month instead of $300).

Second, because your lender already paid the $5,400 bill but only collected $3,600 from you over the past year, your account is short by $1,800. They spread this $1,800 shortage over the next 12 months, which adds another $150 to your monthly payment.

Total increase: Your payment goes up by $300 a month for the next year. Half of that is the permanent new cost of your taxes, and half is repaying the temporary shortage.

If you want to see the exact numbers for your own situation, plug your latest escrow analysis statement into this escrow shortage calculator — it breaks down exactly what changed and when your payment normalizes.

Why New Builds Get Hit Hardest

This shock is most brutal for buyers of new construction homes. If you bought a new build, your initial property taxes were likely assessed on the value of the empty dirt lot. Your lender set up your initial escrow payments based on that low "dirt tax."

A year later, the county reassesses the property with a finished house on it. Your tax bill might jump from $800 a year to $6,000 a year. Suddenly, you have a massive shortage, and your payment skyrockets. If you're building a home, you must budget for the finished tax value from day one, not the dirt value your lender uses at closing. This is a crucial part of calculating

What to Do If You Can't Afford the Higher Payment

If your new payment is unmanageable, you have a few options:

- Pay the shortage upfront: If you have the cash, you can pay the $1,800 shortage as a lump sum. This won't stop your payment from going up entirely (you still have to pay the new higher tax rate going forward), but it will stop the temporary 12-month shortage penalty.

- Request a 24-month spread: If the shortage is severe, call your servicer. Some lenders will agree to spread the shortage repayment over 24 months instead of 12, softening the immediate blow to your budget.

- Dispute the tax assessment: If you believe the county overvalued your home, you can file an appeal with your local tax assessor.

- Shop for new insurance: If skyrocketing homeowners insurance caused the shortage, start getting quotes from other carriers immediately.

When Your Payment Will Go Back to Normal

The good news is that the shortage portion of your increase is temporary. In our example above, the extra $150 a month you are paying to catch up on last year's deficit will fall off after 12 months. Your payment will drop down to just the principal, interest, and the new baseline taxes.

Sources