If you're feeling overwhelmed by multiple credit cards, car loans, or personal debts, you aren't alone. The hardest part of getting out of debt isn't usually the lack of money—it's the lack of a clear plan.

When you just make random minimum payments every month, it feels like the balances never go down. That's exactly why we built the FinanceTact Debt Payoff Calculator. It takes the guesswork out of your finances and gives you an exact "month-by-month" roadmap to freedom.

Here is a quick, step-by-step guide on how to use the tool to build your custom payoff plan today.

Step 1: Gather Your Numbers

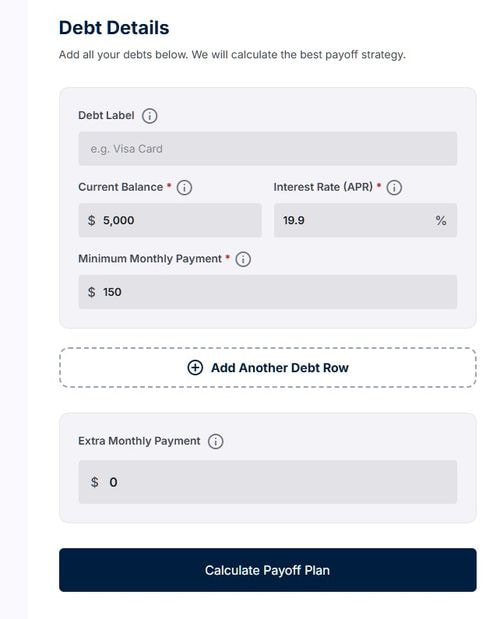

Before you open the calculator, grab your most recent statements. For each debt, you will need:

- Current Balance: How much you currently owe.

- Interest Rate (APR): The percentage you are being charged yearly.

- Minimum Monthly Payment: The lowest amount you are required to pay each month.

Tip: Don't guess! A card with a 24% rate requires a very different strategy than a loan with a 6% rate.

Step 2: Enter Your Debts

Whether you have one credit card or a dozen different loans, the process is the same. Click "Add Another Debt" for every balance you want to track. The calculator works perfectly for a single loan, but its true power shows when you list everything.

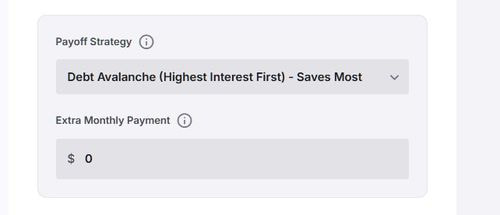

Step 3: Choose Your Strategy

If you added 2 or more debts, a "Payoff Strategy" box will appear. This is where you decide your attack plan:

- The Debt Avalanche: Mathematically targets the most expensive debt (highest interest) first. Saves the most money.

- The Debt Snowball: Targets the smallest balance first for a "quick win." Great for staying motivated.

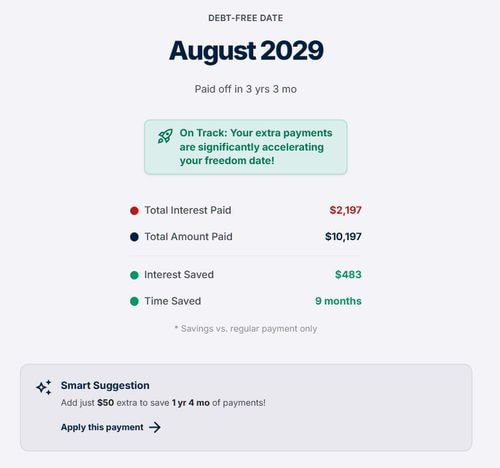

Step 4: Analyze Your Results

As you type, the chart and results panel update in real-time. Look for the Smart Suggestion box—it will suggest the smallest extra payment that delivers the biggest impact for your specific debts.

Step 4: Find Your "Sweet Spot"

Our calculator includes a Smart Suggestion engine. If you're only paying the minimum, look for the suggestion box in the results panel. It will show you exactly how much a small extra payment (like $25 or $50) will shave off your timeline.

🧠 Why is this necessary?

If you've ever wondered why banks only ask for a small "Minimum Payment," you need to read our deep dive:

👉 The Minimum Payment Trap: The Math Banks Don't Want You to Know

Ready to build your plan?

Take 5 minutes, plug your numbers in, and see your exact debt-free date.